|

Home | Search | Browse | About IPO | Staff | Links |

|

Home | Search | Browse | About IPO | Staff | Links |

|

SCRUTINIZE LOCAL OPTIONS With increasing pressure to limit tax increases, many local governments are finding it difficult to meet the demand for services. Federal support continues to decline and many states and cities have been affected by tax limitation initiatives. Thus, communities are being forced to scrutinize local options for additional funding through a more diversified revenue base. One option is user fees. Revenues can be raised by increasing fees currently in existence and by establishing fees for other services where appropriate. A common criticism aimed at user fees is that they are simply an alternative form of taxation; users of fee services are being doubly taxed. However, many services provided by local governments benefit groups including non-property tax paying individuals. In this case, funding a service through general taxation represents a subsidy to the non-tax payer by the tax payers. Other services may be used exclusively by tax payers but the service provides little or no benefit to the general public. In these instances, user fees are justified. User fees are already used to partially fund various services in many communities. Fees are typically assessed for services such as building permits, park and recreation programs, and water and sewer use. Almost all city departments provide some services amenable to user fees. Even police departments charge for some services. For example, fees are often charged for report copies, fingerprinting, and parking violations. The practice of assessing user fees has a number of benefits:

The decision to fund services through user charges raises the question of which services are amenable to fees. Local governments typically charge for special services such as crowd control at special events, or for routine services such as providing copies of various documents. In general, the extent to which a local government can adopt service charge financing depends on the legal ability to levy charges, the availability of other revenue sources and the community's economic and political atmosphere. Decision makers also need to decide at what level, if any, they wish to subsidize each service. To do this, the full cost of each service must be determined. Typical criteria that communities apply in determining whether a service should be funded through user fees or taxes include:

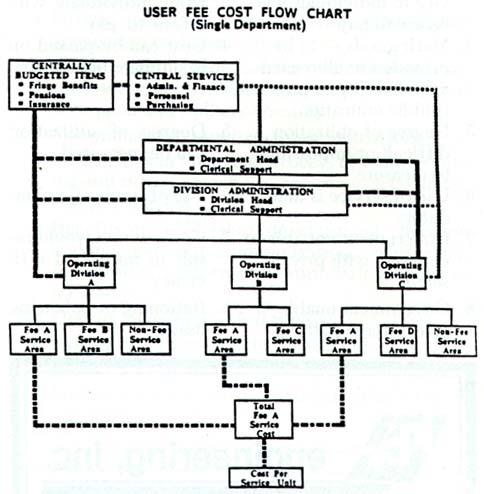

This article was prepared by the staff of David M. Griffith and Associates, Ltd. The firm is headquartered in Northbrook, Illinois and works with more than 1,200 state and local governments each year on a variety of revenue management programs, and has performed nearly 100 user fee studies for states, cities and counties. Geoffrey Johnson, Daniel Denys and Jerrold Wolf contributed to this article. February 1988 / Illinois Municipal Review / Page 7 Most governments tend to set rates, fees, and service charges too low to recover costs. A survey of fifty municipalities across the country, performed by David M. Griffith and Associates, shows that general fund non utility user fee services are subsidized by taxes in the amount of $35 per person. Typically, communities tend to set fees based on those charged by neighboring communities; not on actual costs. These are many different cost concepts which may be used. In establishing service fees, a "fully allocated" cost is often regarded as appropriate. Full costs include direct costs (direct labor, supplies, and equipment used), and a portion of the indirect costs relating to the various departments allocated to the service in an objective manner. Indirect costs include central administration, departmental supervision, support services, and building usage. These costs, while not necessarily related directly to any one service, are necessary to support the delivery of all services. This method of allocating costs is already used by many governments in determining charges to enterprise funds, such as municipal utilities. The accompanying flow chart illustrates the components used in computing the full cost of delivering a unit of service. This approach is used as accounting and management systems are not designed to capture expense data by units of service provided. All expenses, however, need to be documented and accounted for in the analysis. Thus, local managers must carefully identify all of the costs of providing services and correctly allocate them to the actual services delivered.

The total cost of each service includes costs that can be directly identified with the service (found within the operating divisions) and indirect costs in other divisions and departments which must be allocated to the operating divisions. The chart on this page shows a step-by-step allocation approach to determining the cost of a service. This approach is standard for costing government services. From top to bottom, the chart shows the following: • "Centrally Budgeted Items" such as insurance, pension, audits, fringe benefits, and other costs which benefit all departments. Page 8 / Illinois Municipal Review / February 1988 ensure that the total cost of a service area is identified. All three operating divisions have costs associated with the building permit process, they must be added to get the "Total Fee Service Cost." Beyond the basic methodology employed to determine the costs of providing government services, there are application issues that need to be addressed. In some cases, departments provide very few units of some services in any given year. For example, a planning department may only have to deal with a Planned Unit Development (PUD) once every five years, depending on the rate of development in the community. Given this demand, should this service be analyzed? In this case, given the high cost incurred (approximately $19,000 in one instance), a community will be well advised to make this assessment if only to be prepared the next time a large development is proposed. Each service should be analyzed for the potential impact on revenues prior to excluding an area for "lack" of demand. Another issue which needs to be addressed by administrators is what to do with unused capacity. The answer will vary according to the nature of each department. In the case of fire departments, which are basically public safety operations, a large pool of costs will normally be excluded from the analysis of fee generating services. Any uncaptured costs in the inspections department, for instance, are probably related to the inspections function and may be appropriately included in the total costs of providing the various types of inspections. The following Table A shows the situation in one Illinois city. In this case, the city overall was recovering 36% of the costs of delivering 148 different services through current revenues; though the experience of each department varied widely ranging from a 3% recovery (Public Works) to a 88% recovery (Engineering). The Inspections Department was fairly typical in terms of overall recoveries. The Department incurred $156,324 in both direct and indirect costs to deliver six different services with corresponding revenues of $66,486. Thus the overall recovery, in this example, was 43%

The Table B shows the experience of four Midwestern cities of varying populations. In each case, a significant subsidy was found. TABLE B

Local governments across the country have found that basing fees on costs has led to substantial increases in general fund revenues. Even where the towns and cities are making policy decisions to recoup only a certain percentage of the cost of user fee services in certain areas (such as park and recreation programs, senior centers, health centers, etc.) the additional revenue has been significant. The results from the above cities are typical of cities around the country. Local governments around the country are receiving $7,000 to $10,000 in increased general fund revenue per 1,000 population by setting fee levels based on some percentage of cost. With more and more limits being placed on intergovernmental and tax revenues, user fees are one of the best ways to finance governmental services. • February 1988 / Illinois Municipal Review / Page 9

|Home|

|Search|

|Back to Periodicals Available|

|Table of Contents|

|Back to Illinois Municipal Review 1988|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||