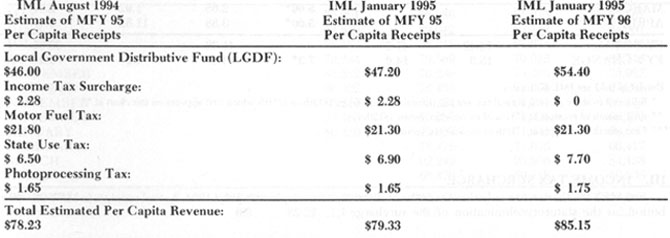

Estimating State Shared Municipal Revenues I. SUMMARY OF FISCAL YEARS 1995 AND 1996 Municipal Fiscal Year (MFY) 1995 (May 1, 1994 - April 30, 1995) has seen faster than projected growth in income tax and sales tax revenues, but lower than anticipated motor fuel tax receipts. Projections made for the first time for Municipal Fiscal Year (MFY) 1996 (May 1, 1995 - April 30, 1996) have incorporated the higher growth rates of the past year, but expect that growth to moderate as we reach the end of a remarkably weak recovery. (Source: IL Department of Revenue/Illinois Municipal League) Current IML staff projections are summarized below;

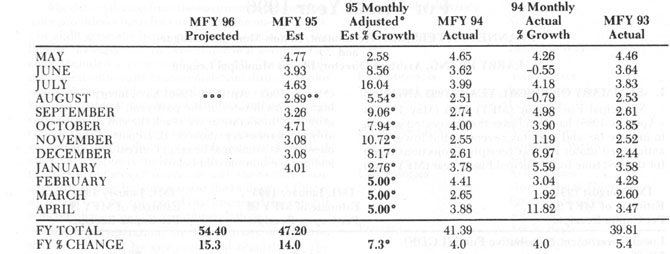

II. INCOME TAX Our last year's estimate of $46.00 per person will be about $1.20 low because the Illinois income tax is growing with the Illinois economy at a rate higher than our 3% projection. Actual receipts in the first eight months reflect an 8.5% increase in the economy plus the effect of the formula increase from l/12th to 1/ llth (a 9.1% increase) beginning with the August, 1994 distribution. Our January, 1995 estimate for MFY 95 is $47.20. For MFY 96, we estimate 5% growth in State income tax revenue. If this is combined with the statutory LGUF formula increase from 1/llth of income tax receipts to 1/l0th which occurs this August (a 10% increase), an overall increase of 15% for MFY 96 is expected. Our January, 1995 estimate for MFY 96 (May 1, 1995 through April 30, 1996) is $54.40. February 1995 / Illinois Municipal Review / Page 17

LOCAL SHARE OF STATE INCOME TAX

Entries in bold are IML Estimates

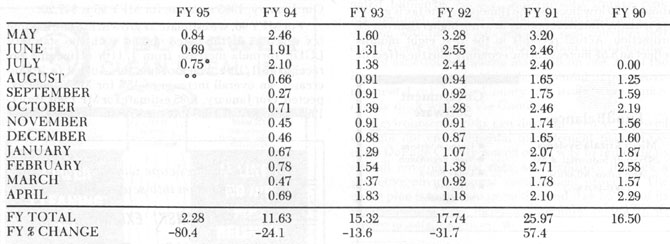

* Reduced to show growth in total tax, not the formula change from l/12th to 1/llth which first appears on this chart at III. INCOME TAX SURCHARGE For MFY 95, there were only three months of distribution, as the statutory elimination of the surcharge took place in July, 1994. Actual receipts in MFY 95 were $2.28.

INCOME TAX SURCHARGE

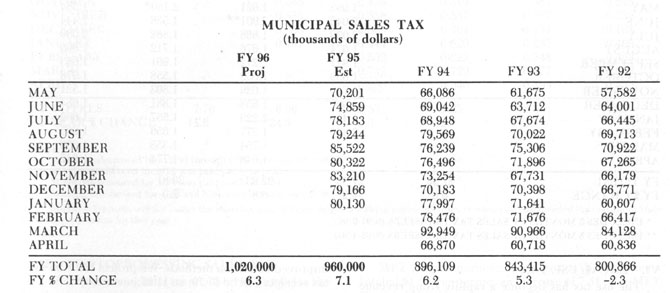

* Last month of ITS distribution Page 18 / Illinois Municipal Review / February 1995 IV. SALES, OR MUNICIPAL RETAILERS OCCUPATION TAX (MROT) MFY 95 receipts of municipal sales tax have been strong, increasing at an 8.1% rate in the first nine months of the fiscal year. We estimate the total for MFY 95 to be $960 million for municipal sales taxes from the 1% Municipal Retailers Occupation, Servicemen's Occupation and Use Tax (titled or registered items only). This represents 7.1% growth from MFY 94. For MFY 96 we estimate total revenue of $1.02 billion, or 6.3% more than MFY 95. Please keep in mind that an estimate of total statewide municipal sales tax revenue is not particularly helpful in your forecast of local sales tax receipts. Your receipts will vary depending on the wide swings in retail sales as stores open and close, or the local economy expands or contracts.

MUNICIPAL SALES TAX

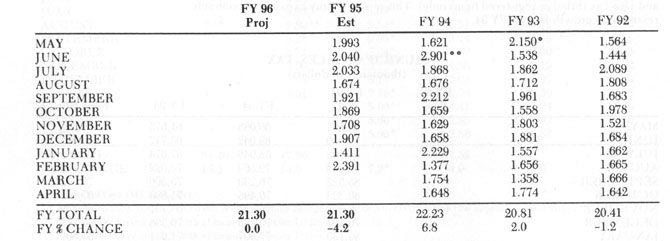

V. MOTOR FUEL TAX (MFT) MFY 95 motor fuel tax revenue is lower than projected, dropping from $22.23 last year to an estimated $21.30 in the year ending 4/30/95. As was described in prior estimates, sales tax transfers in June of MFY 94 contributed to artificially high receipts for MFY 94. For MFY 96, IML staff estimates that MFT disbursements will stay at the same level as this year, or about $21.30 per capita. Motor Fuel Tax revenue has become a static, or even a slowly declining source of per capita revenue for municipalities as average fuel economy continues to improve. In addition, the federal government's efforts under the Clean Air Act have negatively affected this revenue source in two ways. First, Vehicle Emissions February 1995 / Illinois Municipal Review / Page 19 Inspection costs are paid out of gross MFT receipts. Second, federal efforts to impose trip reduction requirements on the Clean Air Act nonattainment areas will also reduce receipts. The only source of growth is the transfer each month of 1.7% of the State sales tax into the State's Motor Fuel Tax Fund as a proxy for the sales tax received from sales of motor fuel.

MUNICIPAL SHARE OF STATE MOTOR FUEL TAX

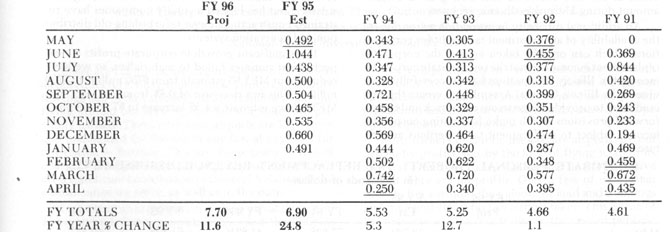

• INCLUDES 5 MONTHS OF SALES TAX TRANSFERS (9/91-9/92) VI. LOCAL USE TAX The use tax has become a rapidly rising revenue source as the Illinois Department of Revenue aggressively attempts to collect use tax on out of state catalog and electronic shopping. The increased state auditing and the voluntary use tax disclosure program appear to have been very successful. MFY 94 produced $5.53 per capita, an increase of 5.3% over MFY 93. MFY 95 receipts to date are running much higher than predicted primarily because of the large June 1994 distribution which was $.57 per capita higher than the June 1993 payment. IML staff has raised its estimate for MFY 95 from $6.50 to $6.90 per capita, a 24.8% increase over MFY 94. MFY 96 revenues should grow with the sales tax, and we believe there is still some uncaptured revenue that will be produced by the Department of Revenue's improved collection methods. We project MFY 96 use tax receipts will be $7.70, an 11.6% increase. Page 20 / Illinois Municipal Review / February 1995

LOCAL SHARE OF THE STATE USE TAX

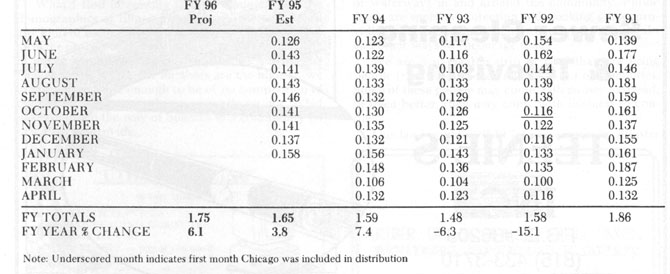

Notes: VII. PHOTOPROCESSING SALES TAX Photoprocessing sales tax receipts run parallel to the estimates for statewide sales tax, as they are a percent- age of total State sales tax receipts, distributed on a per capita basis to municipalities. MFY 94 photoprocessing sales tax disbursements totaled $1.59 per person, an increase of 7.4% over MFY 93. For MFY 95, we estimate $1.65 per person, an increase of 3.8%. For MFY 96, we estimate $1.75 per person, an increase of 6.1%.

LOCAL SHARE OF "PHOTOPROCESSING" TAX

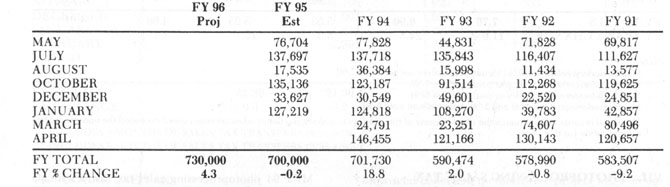

VIII. CORPORATE PERSONAL PROPERTY REPLACEMENT TAX (CPPRT) Since 1979, the Corporate Personal Property Replacement Taxes have been the most volatile and difficult to predict of all state-shared municipal revenues. The reason for this volatility is that over half the receipts come from the additional 2.5% corporate income tax. Corporate incomes fluctuate wildly as corporations February 1995 / Illinois Municipal Review / Page 21 move through the business cycle. Total Illinois corporate profits, and the taxes paid on them can drop as much as 30% in a recession and then grow a similar amount during a strong economic recovery. An additional difficulty in estimation arises due to the availability of an investment tax credit for corporations which can only be taken against the corporate replacement income tax, not the regular State corporate income tax. Illinois corporations have successfully convinced the Illinois General Assembly to create this tax credit and to provide for generous carryback and carryforward provisions which make forecasting corporate income subject to replacement tax a perilous adventure. A measure of stability is found in the other source of replacement revenue, the .8% tax on the invested capital of utility companies. This revenue source has grown steadily, but has lagged as utility companies have restrained constructing new or refurbishing old distribution and generation systems. The significant growth in corporate profits we expected last summer failed to materialize, so we have reduced our MFY 95 estimate from $750 million to $700 million. This is a decrease of 0.2% from last year. For MFY 96, we estimate a 4.3% increase to $730 million.

CORPORATE PERSONAL PROPERTY TAX REPLACEMENT REVENUE DISBURSEMENTS

Page 22 / Illinois Municipal Review / February 1995

|Home|

|Search|

|Back to Periodicals Available|

|Table of Contents|

|Back to Illinois Municipal Review 1995|

|

|||||||||||||||